Most of us do not wake up thinking about payment systems. We just want to buy coffee, order groceries, pay for parking, split dinner, and move on with the day. That is exactly where digital wallets have become so useful. Banks still matter, of course. I use mine for statements, savings, transfers, and anything serious. But for everyday payments, digital wallets often remove the small delays that make banking apps feel slow.

Why digital wallets feel easier in daily life

The biggest difference is simple: a digital wallet is built around the payment moment. A banking app is built around account management. That may sound obvious, but it changes everything. When you open a bank app, you usually see balances, cards, transfers, loans, messages, and security checks. Useful? Yes. Fast at the checkout? Not always. A digital wallet keeps the action close.

You unlock your phone, choose a card if needed, and pay. No digging through your bag. No typing the card number. No searching for the one card you were sure you had yesterday.

And let’s be honest, that moment at the register when people start checking every pocket is never anyone’s finest performance. Digital wallets are also changing how businesses think about payments. The same need for faster checkout, safer payment handling, and smoother account balances appears in many online platforms, including payment-focused products such as crypto casino software. The point is not that every reader uses those platforms. The point is that wallet-style payment logic now appears far beyond simple phone taps at a café.

Speed is the first thing people notice

Digital wallets make payments faster because they reduce the number of steps between wanting to pay and actually paying. In a shop, the process is usually tap, confirm, done. Online, wallet checkout can fill in payment details and sometimes shipping information too. That is a big deal on mobile, where typing long card numbers feels like a small patience test. Here is where wallets usually save time:

- No manual card entry for saved cards

- No need to carry every physical card

- Faster contactless payments in stores

- Easier repeat purchases on websites and apps

Banks can process payments well, but bank apps usually ask you to move through more screens. That makes sense for security and account control, but it is not always ideal when you just want to pay for lunch before your soup gets cold.

Security without making every payment feel difficult

Payment security is one reason people hesitate before using digital wallets. That hesitation is fair. Nobody wants convenience if it creates a bigger risk. But modern digital wallets are not just storing your card number in a pretty app. They often use tokenization, which means your actual card number is replaced with a different payment token during transactions.

Biometric checks also help. Face scan, fingerprint, PIN, or device unlock adds a practical layer of control. I like this because it fits how people already use phones. You do not need to become a security expert just to buy a sandwich. You only need a payment method that checks it is really you before money moves.

Digital wallets reduce online checkout friction

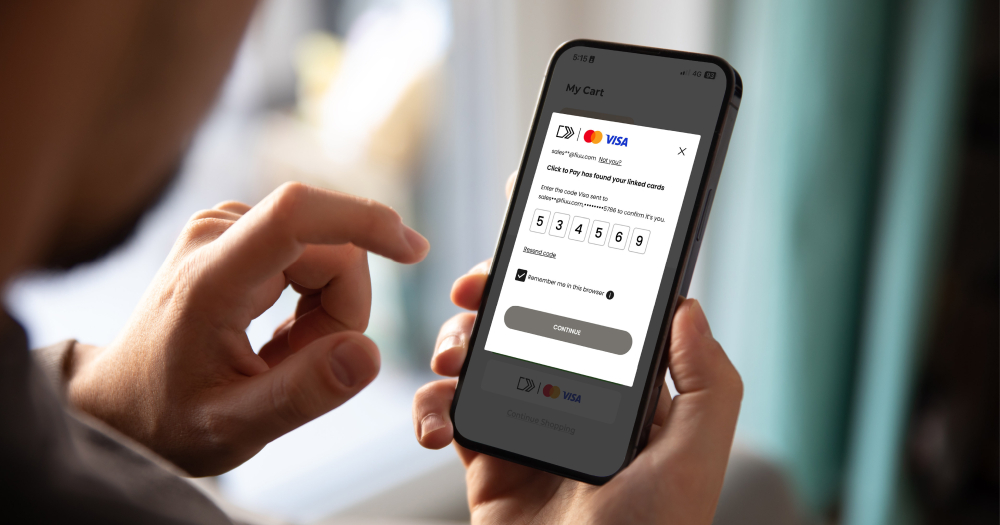

Online checkout is where digital wallets really earn their place. Think about the usual card payment flow. Card number. Expiry date. Security code. Billing address. Maybe a one-time code. Maybe the page reloads. Maybe you mistype one digit and start questioning your eyesight. Digital wallet checkout cuts much of that down. It can store the payment method, speed up authentication, and reduce the amount of information you type into each website.

That matters because many people abandon purchases when checkout becomes too slow or too annoying.

| Everyday task | Bank app experience | Digital wallet experience |

| Buying online | Often needs card details or bank transfer steps | Often uses saved payment details |

| Paying in store | May still depend on physical card | Phone tap can be enough |

| Splitting a bill | May need account details | Often uses contact or phone number |

| Managing cards | Strong account controls | Faster card selection at checkout |

This does not make wallets perfect. Some merchants still do not support every wallet. Some banks have excellent apps. But the wallet’s advantage is clear: it removes repeated typing from repeated payments.

Banks are still better for serious money tasks

A good article on digital wallets should not pretend that banks are outdated. They are not. Your bank is still the place for deeper financial work: savings, loans, statements, direct deposits, large transfers, card disputes, credit checks, and formal records. I would not use a wallet to understand my full financial life. I would use my bank.

That distinction matters because people often compare the two in the wrong way. A bank app is not failing because it has more steps. It has more steps because it handles more sensitive functions. A digital wallet feels easier because it focuses on quick payment completion. In plain terms, one is your financial control room, and the other is your everyday checkout tool.

Everyday situations where wallets beat bank apps

The best way to understand digital wallets is to look at normal days, not technical diagrams. You are buying groceries with one hand full. You are ordering a ride. You are paying for parking while people behind you are waiting. You are buying something on your phone and do not want to stand up to find your card.

Sound familiar? In those moments, digital wallets usually feel easier because they reduce small interruptions.

When you are shopping in person

In-store payments are the classic wallet use case. You unlock the phone, hold it near the terminal, and confirm the payment. It is quick, but the real benefit is consistency. You do not have to remember which jacket has your card. You do not have to hand over a card. You do not have to touch the terminal as much.

When you are paying online

Online, wallets help most when you are on mobile. Small keyboards make card entry annoying. A wallet can let you confirm payment without typing the full card details again. That is not glamorous, but it is useful. And useful wins in everyday payments.

The convenience is also about organization

A digital wallet is not only about cards. Many people also keep boarding passes, loyalty cards, tickets, transport cards, and vouchers in the same place. That makes the phone a small payment and access hub. Is it perfect? No. A dead battery can still ruin the mood. But on most normal days, it keeps things tidy. I especially like this for loyalty cards.

Nobody wants a wallet full of plastic cards from places they visit twice a month. With digital storage, you can collect points, use offers, or scan a pass without carrying extra clutter. The bank app usually cannot do that in the same convenient way because that is not its main job. This is why digital wallets keep gaining ground. They are not trying to replace every financial service. They are trying to make repeated payment moments less annoying. That narrower focus is exactly why they work so well.

What to check before relying on a digital wallet

Before you treat your phone as your main payment tool, set it up properly. Add only cards you actually use. Turn on strong device security. Keep your bank notifications active. Make sure you can remotely lock or erase your device if it is lost. Also, keep one backup payment method. I know, very boring advice. Still good advice. A smart setup looks like this:

- Use biometric login or a strong passcode

- Enable payment alerts from your bank

- Keep your phone software updated

- Carry one backup card when traveling

- Review wallet transactions regularly

The goal is not to be nervous. The goal is to be practical. Convenience is best when it comes with a little common sense.

FAQs

1. Are digital wallets safer than physical cards?

Often, yes. Many digital wallets use tokenization, which replaces your real card number with a device-specific payment token. That means the merchant usually does not receive your actual card number during the payment. Still, keep your phone locked, use biometrics, and turn on bank alerts. Visa and Mastercard both describe tokenization as a way to protect card details in digital payments.

2. What if I lose my phone?

Lock the device remotely as soon as possible, then remove wallet access or contact your bank if needed. A lost phone is not the same as handing someone an unlocked wallet, because payments usually require passcode, fingerprint, or face verification. Do not wait to see what happens. Secure the phone first.

3. Do digital wallets replace banking apps?

No. Digital wallets are better for quick everyday payments, online checkout, loyalty cards, tickets, and small transfers. Banking apps are still better for statements, savings, loans, direct debits, account limits, and formal financial records. The best setup is using both, but for different jobs.

Final thoughts

Digital wallets make everyday payments easier than banks because they are faster, simpler, and built for the exact moment when you need to pay. Banks remain essential for managing money properly, but wallets are often better for daily spending.

If you want fewer card searches, fewer typed numbers, and quicker checkouts, a digital wallet is not just a tech upgrade. It is a practical habit that removes small payment problems from ordinary days.